en

en

da

da

Perhaps, like many others, you find yourself preparing for the upcoming legal requirements for ESG reporting. When reviewing your process and considering various solutions to accommodate these new requirements, you will probably encounter several challenges. We are here to offer guidance and enable you to navigate these obstacles and ensure you an effective reporting process. Therefore, this article gives you six pieces of practical advice that may help in your everyday work with ESG reporting.

It would be an understatement to claim that the CSRD legislation (Corporate Sustainability Reporting Directive) and the related ESRS drafts (European Sustainability Reporting Standards) are easily digested.

The new EU requirements for ESG reporting are comprehensive and meeting them is a major task. Therefore, it makes sense to reflect on what you want from your ESG reporting before deep diving into CSRD.

With CSRD follow new Key Performance Indicators (KPIs), adjustments to existing KPIs and underlying data points, as well as requirements for an auditor’s limited assurance report. This presents a significant challenge for many organisations and, therefore, it is important to be aware of whether you will be in scope of these new reporting requirements, and if so, when. Scope and timing depend on industry, reporting class, and owner structure. Companies in scope of the NFRD (Non-Financial Reporting Directive), which are primarily listed companies, will be subject to compliance already from 2024.

In addition to the interpretation of new legislation in the form of ESRS drafts, some of the significant tasks will consist of obtaining sufficiently high data quality and creating solid internal processes to ensure consistent reporting to enable the required auditor’s limited assurance report.

However, CSRD not only brings challenges but also offers an opportunity to standardise reporting requirements and definitions of materiality across stakeholders. This will ensure greater cross-company comparability and, will likely also reduce the internal workload in this regard.

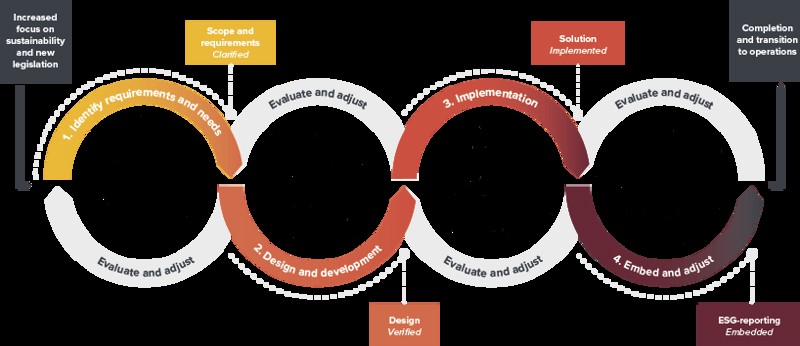

ESG reporting according to Basico’s Change Model

Four-step method and structured approach to identification of requirements and establishment of processes and system.

Six practical experiences you can make use of

1. Basis

Rather than trying to report hastily on EVERYTHING - try to clarify the minimum requirements.

2024 will be the year when many are required to get limited assurance on their ESG reporting for the very first time. And if you are in the process of defining or adjusting your ESG reporting accordingly, you can spend 2023 establishing a solid reporting base and process.

With the new reporting requirements from the ESRS drafts, we advise to begin by identifying the minimum requirements for your company, ensuring that you initially address the necessary reporting needs. Subsequently, you should build a solid basis of established processes covering areas such as data collection, internal controls, guidelines, reporting, and support.

Having this structure in place will also prepare you for the future limited assurance.

Our change model can be used as a method for designing and implementing a basic ESG reporting model.

2. Location

Rather than training colleagues outside Finance in auditing - consider whether ESG should be placed in Finance.

Communication naturally falls under the communication department scope of responsibilities, just as data reporting, controlling, and auditing belongs in Finance. For many years, Finance has refined the processes and discipline that are the prerequisites for an efficient reporting and auditing process and, thus, it could be an advantage to embed the ownership of the ESG reporting in Finance. This ensures that the data and reporting undergo a similar process and quality assurance as financial reporting, which is advantageous for the audit process.

3. KPIs

Rather than assuming that there is internal alignment on new data points and the reporting process - try testing the data quality.

There is no denying that data quality and useability are correlated. Therefore, it is necessary to optimise and work with the data quality, especially because of the novelty of ESG, where interpretations and common understandings are still being developed.

The test reporting phase is likely to reveal areas where data quality needs improvement. This underlines the importance of random sampling of the reported values and the underlying documentation. KPI benchmarks and macro analysis may also help identify any outliers.

Several factors can affect the data quality, common ones being:

- Errors in units of measurement or unit conversions

- Misunderstanding guidelines or lack of training

- Uncertainty about the reporting period or a lack of timely data access

- Incomplete data compared to the reporting scope (such as overlooked electricity metres in a building).

These issues often stem from underestimating the novelty of ESG reporting and the effort required to establish guidelines and ensure data accuracy.

4. Value creation

Rather than considering ESG reporting solely as a compliance exercise - recognise the value of new data.

There is knowledge to be had from ESG reporting: Developments in electricity consumption may reveal trends and optimisation potential across buildings, sites, production machinery, or the like.

Similarly, identifying high employee turnover can highlight an unnecessary loss of knowledge and extraordinary recruitment costs.

Or perhaps you can convert an overview of production emissions into a competitive advantage vis-à-vis new customers or products. Regardless, the emissions from your production are covered by CSRD and form part of the CO2 accounts of your CSRD-covered customers.

Experience shows that compliance requirements can often be combined with valuable knowledge and opportunities for value creation.

5. Cross-organisational cooperation

Rather than thinking that you can solve all tasks independently - leverage the collective expertise of your entire organisation.

ESG reporting requires collaboration across various departments and the knowledge needed for data collection is spread across the organisation, so even if the reporting process in embedded within Finance, the process should involve relevant teams from other departments. For instance, quality or health & safety professionals are subject matter experts for the delivery of input on occupational accidents and sickness KPIs.

Facility management professionals are often experts when it comes to collection of consumption data from sites.

Similarly, legal or compliance professionals can often assist on issues such as whistleblowing and code of conduct.

Make sure to use experts within your organisation.

6. Reporting frequency

Rather than reporting once a year - try to establish a higher reporting frequency.

Waiting until the end of the year to report ESG figures carries unnecessary risk.

Imagine a similar scenario with no ongoing financial reporting throughout the year. More frequent reporting will enable you to follow trends and gives you a chance to correct process or reporting errors during the year.

Moreover, more frequent reporting facilitates change, encourages ownership of processes, and enables focused collaboration with those responsible for reporting.

This can positively affect data quality and availability. Keep in mind that the people responsible for the year-end financial reporting are often the same as those responsible for the ESG reporting. To avoid affecting the year-end closing process by overlapping with a significant portion of the ESG reporting – which can lead to inevitable discussions about guidelines, data, and quality, potentially impacting deadlines for other tasks – having a different timing for ESG reporting could be a solution.

The six above-mentioned points represent general challenges with the establishment or improvement of existing ESG reporting. If you encounter difficulties with your company's ESG reporting and require guidance or assistance during implementation, Basico is here to help.

Mette Slipsager and Morten Virenfeldt

ESG trends in 2025

Currently, ESG is developing rapidly, while at the same time covering a wide span of issues. Some of the issues on our radar in 2025 are:

- ESG reporting with business value

- Automation of ESG IT platforms

- ESG assurance readiness

- The VSME standard

- Pay transparency directive

- Extended producer responsibility for packaging

- Greenwashing og Green claims

ESG reporting at its best

Now, you can get access to advice (in Danish) about the effective ESG reporting process directly in your inbox. We have combined the most recent guidelines on ESG reporting with our knowledge about processes, methods, design, and the embedding of ESG into one focused for you to get a hold of already now.

Are you in control of your ESG set-up?

Two of the areas presenting problems in many companies in connection with ESG reporting are establishment of a working operating model and securing the desired data quality. We at Basico can help you with both ESG data capture and the creation of an ESG operating model.

Please don’t hesitate to contact us for a talk about how we can help you and your company.