en

en

da

da

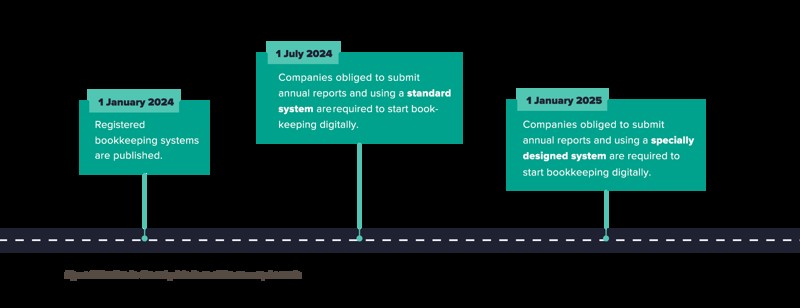

Soon the calendar says 2024, and it’s time to wave goodbye to manual bookkeeping processes and the storage of physical documentation. Because in July 2022, the Danish Parliament (Folketinget) decided that future bookkeeping must be digital. For many companies, this means upgrades of existing systems or implementation of new ones. Read on as we delve into the new bookkeeping act to ensure that your company is compliant.

The new bookkeeping act introduces stricter requirements for bookkeeping systems and bookkeeping methods as well as for IT security and process automation. And even if your company does not use Excel-based accounting systems, we would appreciate having your attention for a while longer. The amendment of the act will affect all companies – no matter whether they use a stand-alone bookkeeping system or an ERP system with a fully integrated bookkeeping feature.

Consequently, many companies will experience great challenges meeting the new requirements – especially those having rather old systems that are not cloud-based.

This article gives you an overall presentation of the most important requirements to give you an idea of 1) what is required from your existing system and 2) whether you need to upgrade to a completely new system and how you get started (cf. figure 1).

The new bookkeeping act contains as many as 38 paragraphs and, therefore, we will focus on the most important amendments that you need to be familiar with:

- Requirement to use a digital bookkeeping system

- Requirement to store documents digitally

- How does the distribution of responsibilities look?

Requirement to use a digital bookkeeping system

The new bookkeeping act has made it mandatory for companies to use digital bookkeeping systems to record transactions and to store both recordings and invoices.

Historically, companies have not been required to use a specific type of bookkeeping system. Therefore, you need to know the difference between standard and specially designed systems since this is essential to understanding the new bookkeeping act. The fact is that the act introduces amendments that may require new technical and organisational adjustments in the company going forward.

The bookkeeping act distinguishes between two types of digital bookkeeping systems that you can use:

- A standard system: A generically constructed system, marketed and sold on the Danish market on equal terms. General subscription and license terms apply to everyone, and the system must have been registered with and approved by the Danish Business Authority.

- A specially designed system: A system designed specifically for an individual company on individual market terms. It may be a rather old standard system that is no longer supported by a provider and that is, therefore, further developed by the company itself or by a third party.

All digital bookkeeping systems must meet the following requirements no matter whether they are standard or specially designed systems:

- Support continuous recording of the company’s transactions as well as digital storage hereof with related invoices covering a minimum of recent five accounting years.

- Comply with recognised IT security standards, including user and access management as well as automatic back-up of recordings and invoices. The back-is compliant if the systems used are:

-

- Cloud-based bookkeeping systems where transactions and invoices are stored in the cloud.

- Hybrid-based bookkeeping systems where the system is installed on a locally placed server and has a functionality for automatic storage of recordings and invoices with a third party.

- Specially designed bookkeeping systems where system, recordings and invoices are placed locally and where a back-up of the entire system is taken continuously for storage with a third party.

- Meet requirements for automation of companies’ administrative bookkeeping processes. This means that the system must make it easier to standardise information submitted to/from public authorities or a third party. This entails, i.a., automatic e-invoice submission and receipt, compliance with standard data formats, a possibility of bookkeeping using the standard chart of accounts of the Danish Business Authority, or a possibility of mapping the company’s existing chart of accounts according to this.

Requirement for digital storage

The current requirement to store company invoices and other documentation is expanded. This means that, in the future, digital storage must be part of the bookkeeping system. This makes it possible to search for and find documentation of each individual transaction. So far, the digital storage obligation applies only to receipts of purchase and sale.

How does the distribution of responsibilities look?

As a consequence of the bookkeeping act, the placing of the responsibility for meeting the mandatory requirements depends on whether you have an approved standard or a not approved standard/specially designed system.

The Danish Business Authority expects to publish a list of approved, digital standard bookkeeping systems on 1 January 2024. Today, a wide range of digital standard bookkeeping systems and ERP systems are available from the Danish market, including Microsoft Business Central, Microsoft Dynamics 365, e-conomic, and many others. If you use an approved standard system that figures on the list of the Danish Business Authority, you can leave the responsibility with the system provider and the Danish Business Authority.

If, on the other hand, you use a specially designed system, it is the responsibility of the company that the bookkeeping system complies with the provisions of the bookkeeping act. You should also be aware that the Danish Business Authority expects to publish an executive order towards the end of 2023 stipulating more specific requirements for specially designed systems.

Our expectations of the new bookkeeping act

It will be a commercial requirement for all existing standard bookkeeping and ERP systems that they meet the new provisions and, thus, are registered with the Danish Business Authority. Therefore, it is expected that a great number of the existing standard solutions available from the market will be approved and that the need for assessments, adjustments, and upgrades will be kept at a minimum for companies using these system solutions.

However, there is concern about specially designed, not cloud-based systems – both bookkeeping and ERP systems – since it may be challenging, if not impossible, to comply with all the requirements. It may, for example, be challenging to ensure approved back-up procedures, to guarantee role and access management, and to lock the access to deleting or editing already booked transactions. Specially designed systems pose a greater risk since they are no longer supported by the original system provider and are, therefore, often maintained and coded by the company itself via its own developers or third-party developers from specialised IT companies.

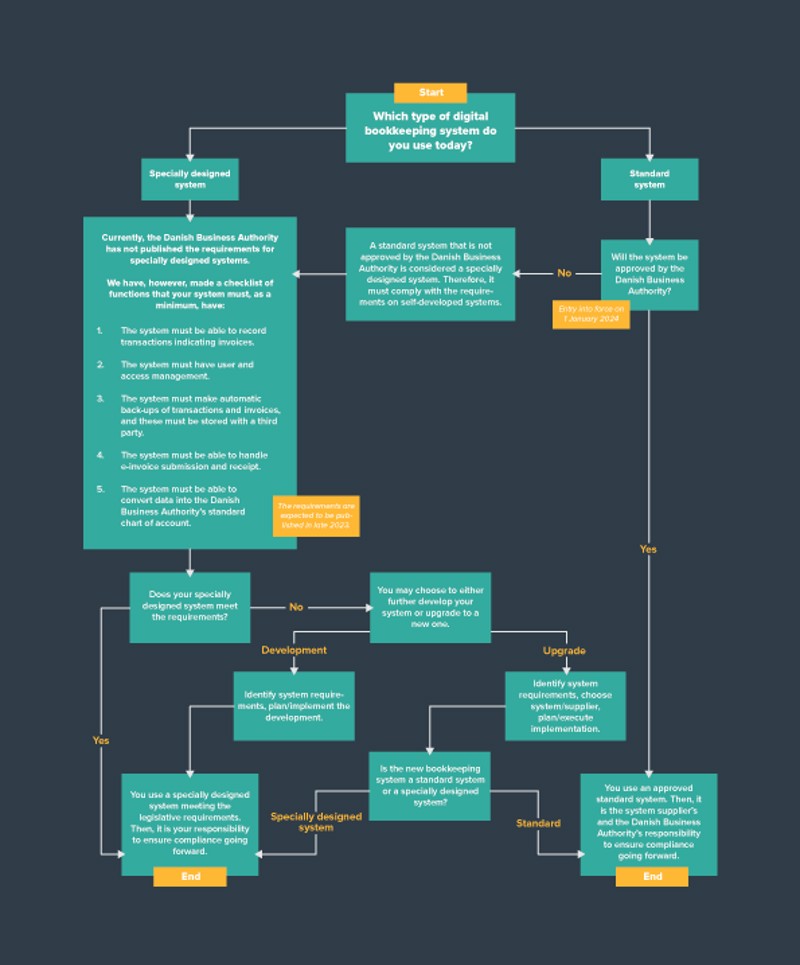

If in doubt about your company’s situation, have a look at our decision tree that gives you answers to the most important questions:

- Do you have a standard system compliant with the requirements of the bookkeeping act?

- Do you have a specially designed system that needs further development to be compliant with the mandatory requirements?

- Do you have an outdated, specially designed system so that you should invest in a new one?

Are you in doubt about your current system’s category?

Since we are continuously updated on the most recent requirements of the Danish Business Authority and are in close dialogue with a number of system providers, we can help you define to which category your bookkeeping system belongs. We will have a look at your existing bookkeeping system and whether it’s an on-premise or a cloud-based solution. By far most cloud-based solutions will most likely be included in the register of approved standard systems. If, on the other hand, your bookkeeping system is an on-premise solution – such as a rather old version of Microsoft (for example Navision, NAV, Axapta, AX, etc.), SAP (R3, ECC, etc.), and Oracle (JD Edwards), you should consider it specially designed and, subsequently, assess whether it can meet the requirements – perhaps together with an external third party.

Often, we can – through a pre-analysis – implement the changes needed to ensure that your bookkeeping system is compliant.

No matter which solution model you use, you should always consider the economic investment and the subsequent maintenance costs in the light of the functionality, the degree of future-proofing of the business strategy, the dependency on support, the division of responsibilities, etc.

Are you in doubt about your company’s situation? Get help from our decision tree below.

Do you need to upgrade to a new standard ERP system?

Have you reached the conclusion that it is either not technically possible or, for example, economically expedient to adjust your existing bookkeeping or ERP system to the new requirements? Then, you need to start a process choosing a system and a supplier.

The new bookkeeping act may involve both technical and organisational changes for many companies, but – though the requirements for digital bookkeeping may seem much to swallow – we recommend that you consider the new legislation an occasion for increased digitalisation of your company’s processes. In the long term, it may result in increased efficiency and accuracy of the accounting processes, improved data accuracy and traceability, time and cost savings, as well as improved IT security.

Read this and more articles (in Danish) in our magazine Content here.

Competences – full-circle

When helping a Finance function digitalise and automate, we take pride in combining the applications and tools that will meet your specific demands. In a way so that the solution supports the data, processes and people working hard behind the lines.

Basico's digitalisation circle

Do you need assistance to assess your systems?

We have vast experience analysing and documenting companies’ system requirements as well as which ERP systems will support recent legislative requirements.

We can help you operationalise a wide range of finance applications and finance processes, such as role and responsibility management, OCR solutions for invoice digitalisation, cloud-based back-up solutions, automation of financial processes such as O2C, P2P, etc. by means of Power Apps, Workflows, RPA, etc.

In other words, you won’t have to worry if you need help to move on.